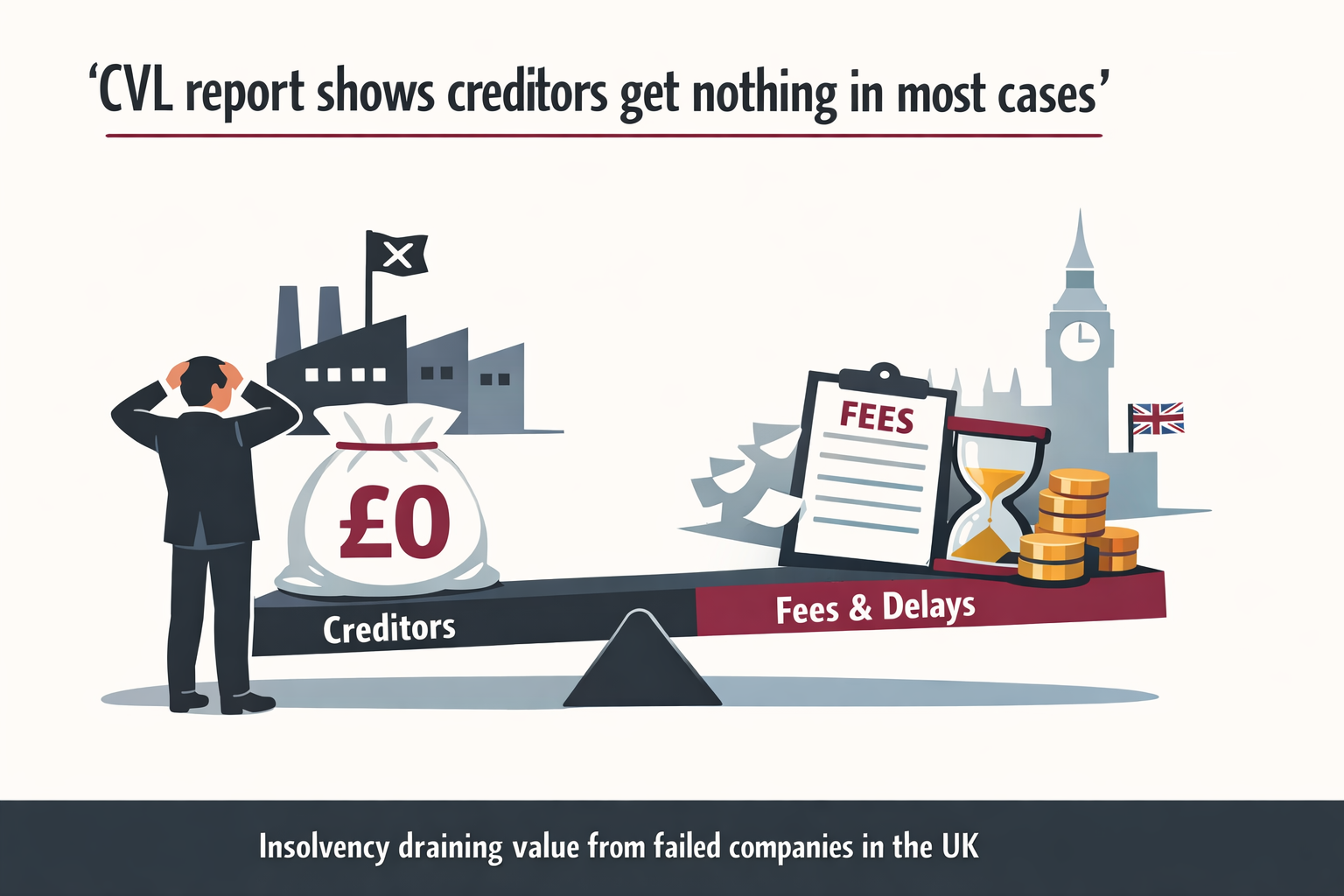

The most damaging indictment of the UK’s creditors’ voluntary liquidation regime did not come from an angry former director or a campaigning creditor. It came from the Insolvency Service itself. Its December 2024 CVL research report, based on 2,717 completed liquidations sampled from cases that began in 2017, found that in 86% of cases no creditor class received any payment at all. The median recovery for unsecured creditors was 0%. The median length of a case was 712 days. The median total fees were £12,937 against median asset realisations of just £5,798, and the median cost of the process came out at 163% of the value of the estate. The state’s own conclusion was that a process taking about two years while delivering zero recovery to most creditors is, at the very least, difficult to defend as efficient. (gov.uk) That matters because CVL is not some obscure corner of the corporate system. It is the main exit route for failed companies. When the official evidence says the process usually produces nothing for creditors, yet still consumes time, money and professional fees, creditors are entitled to ask a blunt question: what, exactly, is this machinery for? On the government’s own numbers, it is not primarily returning money to those left unpaid. (gov.uk)

The fee structure is where the creditor’s problem becomes impossible to ignore. The same report found that 83% of sampled cases involved pre-appointment fees, with a median pre-appointment payment of about £4,000. In other words, money is commonly extracted before the formal liquidation has even started. The report also found that in 14% of cases there were no assets realised at all, and in 70% recoveries were below £10,000. Yet the system still moved forward, still generated paperwork, and still imposed cost. (gov.uk) The Insolvency Service did not find that every pound realised went to practitioners. It found a median post-appointment payment to IPs equal to 21% of assets realised, while the median amount paid to creditors as a share of assets realised was 0%. That distinction matters, because the profession often defends itself by pointing to the statutory order of distribution and the poverty of many estates. Both points are true as far as they go. They still do not answer the creditor’s complaint. A statutory process that routinely starts with too few assets, absorbs cost, and ends with nil return is still a failed process from the creditor’s side of the table. (gov.uk)

If ministers had treated the CVL report as a warning flare, the argument might already have shifted. Instead, the market it described is still running at scale. In 2024 there were 18,840 CVLs in England and Wales. In 2025 there were 18,525. The past four years have been the four highest annual CVL totals since the series began in 1960. In 2025, one in 190 companies on the effective register entered insolvency. This is not a legacy problem that has quietly burned out. It is a live-volume system still sending companies into terminal liquidation in extraordinary numbers. (gov.uk) That volume matters because scale changes behaviour. A procedure designed in law as a careful winding-up process begins to look, at market level, like a production line. The Insolvency Service’s own report acknowledged concern about so-called CVL factories and burial liquidations. It recorded the worry in plain terms: low-fee, high-volume offerings raise the question of whether full statutory duties can really be carried out for the price advertised. That is not a hostile outsider’s slogan. It is the government recording what the market has become. (gov.uk)

The report went further and placed one of the sharpest parliamentary criticisms directly on the record. It quoted Lord Agnew’s description of an 'unholy trinity' of company director, local accountant and 'friendly' insolvency practitioner quietly liquidating a company without proper questions being asked about value removed before the collapse. That passage will irritate the profession, but it is in the Insolvency Service’s own report because the concern is real enough to merit official notice. (gov.uk) What is striking is that the report did not entirely dismiss those fears, even where its statistical findings were more cautious. It found that 73% of sampled cases involved total payments to the IP of less than £10,000. It also found a statistically significant association between lower fees and lower sift-in rates, although the effect size was small. The official line was measured. The creditor’s reading will be harsher: if most cases are cheap, asset-poor and concluded with nothing to distribute, the commercial pressure is towards speed and throughput, not stubborn investigation on behalf of people already unlikely to see a penny. (gov.uk)

The structural conflict at the centre of CVL has still not been honestly resolved. Under rule 6.14 of the Insolvency Rules 2016, directors send creditors notice seeking a decision on their nominated liquidator, and the decision date can be set as little as three business days after the notice is delivered. If the objection threshold is not met, deemed consent follows. The law preserves a creditor right to object, but in small-company failures with fragmented trade creditors and almost no time to organise, that right is often more theoretical than practical. (legislation.gov.uk) Once appointed, the liquidator is under a legal duty to report on the conduct of the directors to the Secretary of State, in practice the Insolvency Service. That is where the arrangement begins to look backwards. The office-holder is commonly brought in through a process driven by the directors, paid in part through pre-appointment fees, and then expected to assess the same directors’ conduct with sufficient independence and intensity to protect the public interest. The CVL report confirms that every such case sits inside the conduct-reporting system. That is not a design that inspires creditor confidence. (gov.uk)

The outcomes of that conduct regime are revealing. In the sample reviewed by the Insolvency Service, 54% of cases were sifted in as in scope for investigation, but only 10% were targeted for further investigation, and only 5% of the total dataset resulted in a director disqualification. Where time-cost data existed, the median investigation time was seven hours out of a total median of 48 hours on the case, or 15%. Again, none of this proves that office-holders are failing to do their job in every file. It does show that in the typical CVL, investigation is a relatively small slice of the work charged. (gov.uk) For creditors, that is the point at which confidence gives way to doubt. They are asked to accept that liquidation is a formal process of scrutiny as well as asset realisation, yet the median case produces no recovery, limited investigative time and no sanction against the directors. The government’s own report says the current process may be viewed as ineffective in relation to creditor outcomes. It is hard to see how a creditor reading that sentence could disagree. (gov.uk)

The regulation built around this market does little to calm those concerns. The Insolvency Service’s 2021 consultation said the current structure of four recognised professional bodies plus an oversight regulator no longer provided an effective framework, referred to a perception of lack of impartiality, and warned about regulatory arbitrage. Yet the September 2023 government response stopped short of creating a single regulator. Ministers said there was scope for improvement without taking that step and promised to work with the RPBs on 'significant and measurable improvements' instead. (gov.uk) By 1 January 2025, following Chartered Accountants Ireland’s exit, the number of recognised professional bodies in Great Britain had in practice reduced to three: ICAEW, the IPA and ICAS. The same annual review recorded 1,504 authorised insolvency practitioners at that date. It also noted that the IPA had changed its articles, effective 1 January 2025, to restore a clearer separation between membership and regulatory functions. That change was welcome, but it was also an implicit admission that the old arrangement had become hard to defend. The government knew the model was under strain, yet still chose incremental repair over root-and-branch reform. (gov.uk)

The complaints data shows why creditors remain sceptical. In 2024 the Insolvency Service’s Complaints Gateway received 656 complaints. Only 144, or 22%, were referred to the recognised professional bodies. Another 289, or 44%, were closed. More than 70% of those closures were because the complainant did not provide further evidence or information. Across the profession, the annual review recorded 63 published sanctions in 2024. The same review states that the Insolvency Service considered only two complaints about the RPBs themselves, and neither was upheld. (gov.uk) Those figures do not prove widespread wrongdoing by practitioners. They do show a system that is hard for complainants to penetrate and slow to produce visible accountability. Creditors dealing with a nil-return liquidation are expected to understand a specialist process, gather evidence from inside a file they usually do not control, and then persuade a structure still rooted in professional self-regulation to act. That is a high bar for any unsecured creditor, let alone a small supplier already out of pocket. (gov.uk)

It is also wrong to present CVL as a clean shield for directors. The liquidator’s reporting duty is mandatory. The Insolvency Act still allows action for misfeasance under section 212, wrongful trading under section 214, and preferences under section 239 where the facts justify it. The government’s own enforcement material shows that formal insolvency remains a gateway into scrutiny, not a safe house from it. (gov.uk) In 2024-25, official enforcement data recorded just over 1,000 director disqualifications, with an average disqualification tariff of 8.3 years. The annual report also recorded 118 compensation orders or undertakings worth a combined £3.6 million, alongside 51 criminal prosecutions linked to Covid financial support scheme misconduct, 19 of which resulted in imprisonment. Whatever some marketing copy may suggest, formal liquidation is not a magic scrub of director liability. It creates the reporting trail that can end in bans, compensation and, in the more serious cases, prison. (gov.uk)

The case for reform becomes stronger when compared with what the system does not use. In 2024 there were only 202 company voluntary arrangements against 18,840 CVLs. By the end of 2022-23, HMRC was managing £5.7 billion of debt through 912,000 Time to Pay arrangements, and around 90% of those arrangements were completing successfully. Meanwhile, the government’s own evaluation of the restructuring plan said it was seen as too costly and time-consuming for the SME market. By 31 December 2025, only 57 restructuring plans and 67 moratoriums had been registered at Companies House since those CIGA tools were introduced in June 2020. Rescue tools exist on paper. The traffic still flows overwhelmingly towards liquidation. (gov.uk) That leaves a glaring policy gap. A company that can lawfully strike itself off may do so online for £13, or £18 on paper, at Companies House. But an insolvent small company with modest debts and little cash sits in a more punishing space: too poor for a value-preserving restructuring, too risky for informal drift, and pushed towards a CVL market that the Insolvency Service’s own data says usually returns nothing to creditors. That gap is where the current system earns its money. (gov.uk)

There is also a cultural failure running through the official material. In its confidence research, the Insolvency Service recorded that debtors and insolvency practitioners alike said stigma around insolvency prevents people seeking help earlier, and that IPs believed the same problem extended to corporate directors, who delay until a company is no longer viable. The same research found that debtors and directors often begin the process with only a limited understanding of the regime and of the options available. A serious rescue framework cannot work if the first meaningful contact comes when the business is already beyond repair. (gov.uk) That should have pushed policy towards earlier intervention, simpler restructuring routes and genuinely independent oversight. Instead, government has spent years documenting the weaknesses, consulting on them, and then stepping back from the deepest reform. Creditors are left to watch case after case move through a process the state now admits is poor at returning money, expensive to run and only patchily effective at public-interest scrutiny. The profession may object to the language. It is much harder to object to the figures. (gov.uk)