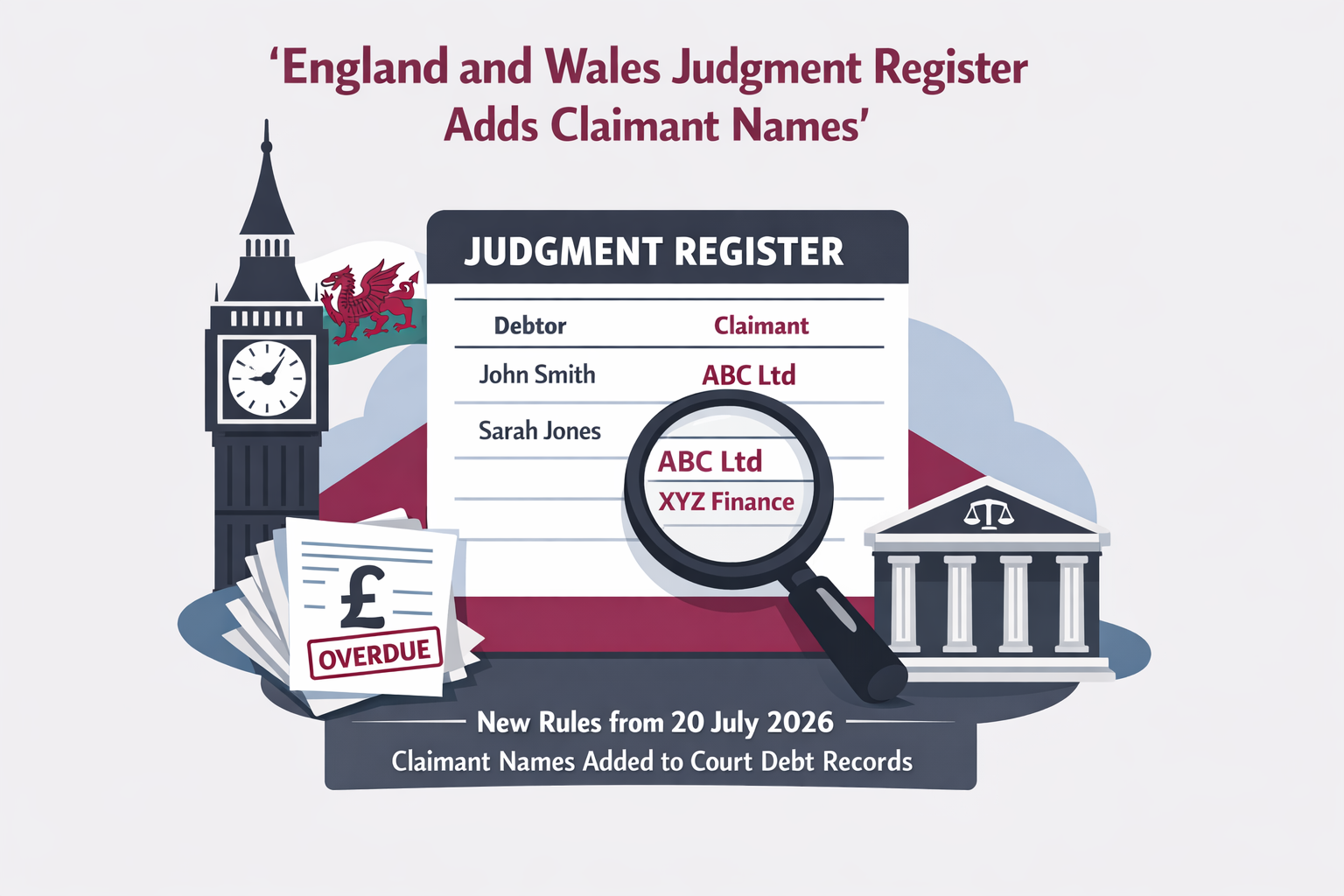

A quiet change to court record-keeping in England and Wales is about to make unpaid debt judgments easier to scrutinise. The Register of Judgments, Orders and Fines (Amendment and Transitional Provision) Regulations 2026 were made on 23 June 2026, laid before Parliament on 29 June 2026 and come into force on 20 July 2026. On paper, this is a narrow amendment to the 2005 regulations that govern the register. In practice, it closes a blind spot. For creditors, insolvency office-holders and anyone examining financial distress before a collapse, the public record will begin to show not only that money is owed under a judgment, but who brought the claim in the first place.

The key amendment sits in regulation 10 of the 2005 scheme. According to the statutory instrument published on legislation.gov.uk, the return sent by the appropriate court officer must now include the full name of the claimant for whom the entry is to be made on the register. That new requirement is inserted as regulation 10(1)(aa). That matters because a judgment entry without a claimant name can leave too much guesswork in the system. A county court judgment may signal pressure on a company or individual, but without the claimant field, observers have had less chance of seeing whether the debt came from a trade supplier, a finance house, a debt purchaser, a landlord or some other repeat claimant. In insolvency work, that missing context can slow down even basic questions about who was pressing for payment and when.

The change is not universal. The new claimant-name requirement does not apply where the claimant has court-ordered anonymity under rule 39.2(4) of the Civil Procedure Rules 1998, or anonymity granted by statute. That is an obvious safeguard and one few would dispute. More striking are the other carve-outs. The amendment does not apply to administration orders made under section 112 of the County Courts Act 1984, nor to tribunal awards from the First-tier Tribunal, Upper Tribunal, employment tribunals or the Employment Appeal Tribunal where money is payable. For an insolvency-focused readership, it is worth being clear that these administration orders are a county court consumer debt process, not corporate administrations under the Insolvency Act 1986. Even so, the exclusions mean the new transparency still stops short of a full picture across every money award that may signal distress.

The Ministry of Justice has also built in a delay before the claimant names appear on the public register. Regulation 3 creates a transitional period beginning on 20 July 2026 and ending on 19 October 2026. During that window, returns can be received by the Registrar, but the Registrar is not yet required to record the claimant’s name on the register. In plain terms, the data starts flowing from 20 July 2026, but publication of claimant names on the register is pushed back until 20 October 2026. That three-month gap may sound technical, yet it is the sort of detail that matters to anyone expecting immediate visibility. Credit managers, investigators and distressed-debt watchers will not see the full benefit on day one.

The explanatory note says no full impact assessment has been prepared because no, or no significant, effect on the private, voluntary or public sector is foreseen. That deserves a more sceptical reading than the note offers. Changing what appears on a public court debt register is not a cosmetic step when businesses, lenders, trade creditors and insolvency professionals use those records to assess payment risk and patterns of enforcement. Adding claimant names may help expose repeat use of litigation by connected parties, reveal when a distressed company is being pursued by one dominant creditor, and make it easier to distinguish ordinary supplier disputes from concentrated pressure by debt purchasers or finance firms. None of that turns the register into a complete investigatory tool, but it does make the public record more useful for anyone trying to understand how a debtor’s position worsened before formal insolvency or enforcement action.

There are still limits. The amendment does not change the underlying judgment process, does not remove anonymity protections, and does not bring the excluded tribunal routes into view. It also says nothing about how searchable, consistent or user-friendly claimant data will be once publication begins. As ever with public records, the value lies not only in what is collected but in whether it can be checked, matched and read without specialist workarounds. Still, this is a meaningful shift. A register that identifies both the existence of a money judgment and the party behind it is better suited to scrutiny than one that records only half the story. For creditors following deteriorating payment behaviour, and for insolvency investigators piecing together pressure points before failure, the July 2026 amendment is modest in form but useful in effect.