Strip away the official language and one pattern keeps repeating in British insolvency: those furthest down the queue rarely see a penny. The Insolvency Service’s own research into creditors’ voluntary liquidations (CVLs) shows 86% of cases made no payment to any creditor and the median cost of the process ran to 163% of the estate. In short, the pot is usually empty before unsecured creditors get a look in.

This didn’t happen by accident. Since the Insolvency Act 1986 pushed the system onto licensed insolvency practitioners (IPs), supervision has largely been delegated to professional bodies, with the Insolvency Service sitting above them as oversight regulator. That arm’s‑length model has left the profession policing much of its own conduct, and it is one reason large firms continue to dominate headline appointments.

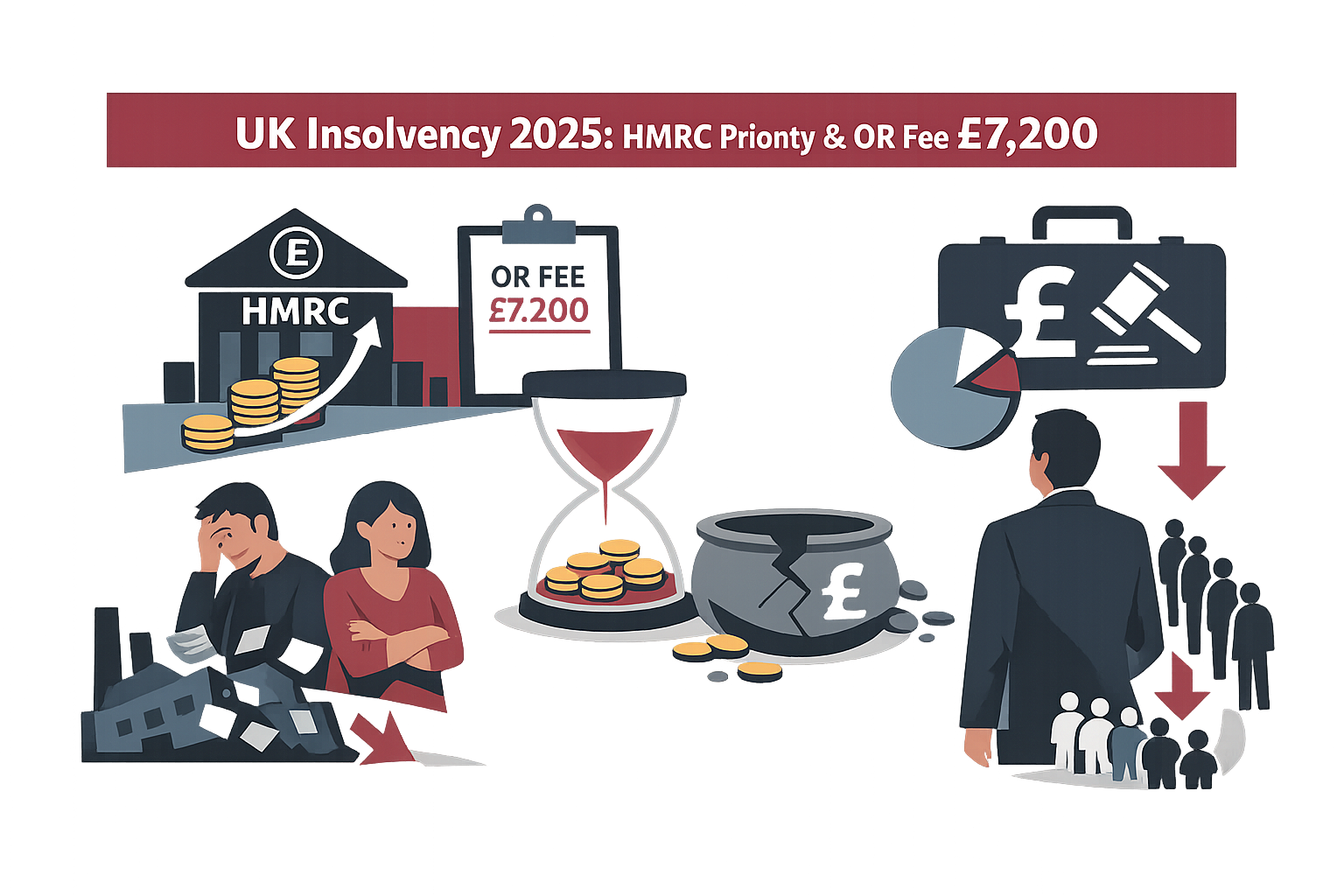

Meanwhile, the state takes its cut up‑front. From 9 January 2025, the Official Receiver’s fixed general fee rose to £7,200 per case, with a further 15% charged on assets realised where the Official Receiver is trustee or liquidator. Ministers defend this as cost recovery; creditors see a statutory skim that bites before distributions are even contemplated.

HM Revenue & Customs has also moved up the ladder. Since 1 December 2020, HMRC enjoys secondary preferential status for certain taxes (VAT, PAYE, employee NICs). That puts the tax authority ahead of floating‑charge holders and unsecured creditors. The Treasury’s own material flagged the intention clearly; industry analyses estimated the change would net the Exchequer around £185m a year, though later data suggested the actual uplift was far smaller. Either way, it means there’s less left for everyone else.

Officials point to 2015 fee reforms and a revised SIP 9 as fixes for conflicts around remuneration. Those changes forced IPs to present fee estimates and made them subject to caps unless creditors agree otherwise. Yet the Insolvency Service’s 2024 CVL study shows the basic outcome hasn’t shifted: the median return to unsecured creditors remains zero, and process costs often overwhelm estates. Transparency without effective leverage is not control.

Talk of a ‘rescue culture’ also jars with the numbers. In 2024, 79% of corporate insolvencies were CVLs and 14% were compulsory liquidations; administrations accounted for 7% and CVAs less than 1%. On any reading, the UK remains a closure‑first regime, with liquidation the default route for distress.

When failures turn high‑profile, the beneficiaries are familiar. The parliamentary report into Carillion recorded how PwC, appointed as Special Manager, invoiced more than £20m in the first eight weeks, while MPs criticised the Big Four’s pervasive, lucrative roles before and after collapse. Creditors and pensioners were left waiting.

On enforcement, the government has leaned heavily on directors. In 2024–25, 1,036 directors were disqualified, 736 for Covid loan abuse, with average bans around eight years. During the pandemic, ministers temporarily suspended wrongful trading to avoid premature shutdowns, but the suspension ended in April 2021 and the deterrent returned. The message is clear: get judgments wrong and expect personal sanction.

Crypto now adds a new layer of complexity. The Digital Securities Sandbox took effect on 8 January 2024 to let regulated market infrastructure test blockchain‑based issuance, trading and settlement. In April 2025, HM Treasury published a draft order to bring “qualifying cryptoassets” and “qualifying stablecoins” into the Regulated Activities Order; the FCA followed with proposals on fiat‑backed stablecoin issuance and crypto custody, while the Bank of England consulted on the regime for systemic stablecoins. For insolvency outcomes, that means more client‑asset style rules, sharper safeguarding obligations, and a clearer failure toolkit for operators that could once have fallen into procedural gaps.

London is also arming investigators to seize digital value at speed. The Economic Crime and Corporate Transparency Act 2023 gives agencies fresh powers to freeze, forfeit-and in limited cases destroy-cryptoassets, with operational guidance issued in April 2024. If a company’s tokens are detained under these powers, that is value that may never re‑enter the estate for the benefit of creditors.

For payment and e‑money firms, a bespoke special administration has existed since 2021 with a statutory objective to return customer funds promptly. Government plans now extend a similar, FMI‑style special administration approach to “digital settlement asset” firms once systemic. That matters: where client funds or crypto are held on trust, they sit outside the insolvent estate; where they are not, unsecured creditors stand at the back as usual.

Even reforms marketed as pro‑creditor can have muted effects. The ‘prescribed part’ ring‑fence for unsecured creditors was increased from £600,000 to £800,000 in 2020, but the later restoration of Crown preference diluted floating‑charge recoveries further and reduced room for consensual rescues. Rescue needs aligned incentives; current rules still pull in the other direction.

Against this backdrop, unsecured suppliers and employees remain the shock absorbers of failure. The system pays office‑holders and prioritised claimants first; HMRC’s upgraded status adds another mouth to feed; and the state’s own fees are deducted before distributions begin. The Insolvency Service’s CVL data confirms what trade creditors experience daily: most cases deliver nothing back.

So what should stakeholders do? Creditors should demand robust, comprehensible SIP 9 fee information and use their statutory rights to question remuneration; organise collectively rather than acting alone; and, in crypto‑exposed collapses, scrutinise whether assets were properly safeguarded for clients or pooled on the balance sheet. For directors genuinely trying to trade through distress, keep full board records of viability assessments and advice taken-especially now that wrongful trading protection has lapsed and stablecoin or crypto‑asset exposures carry novel safeguarding duties. The tools exist; the leverage rarely does unless creditors insist on it.